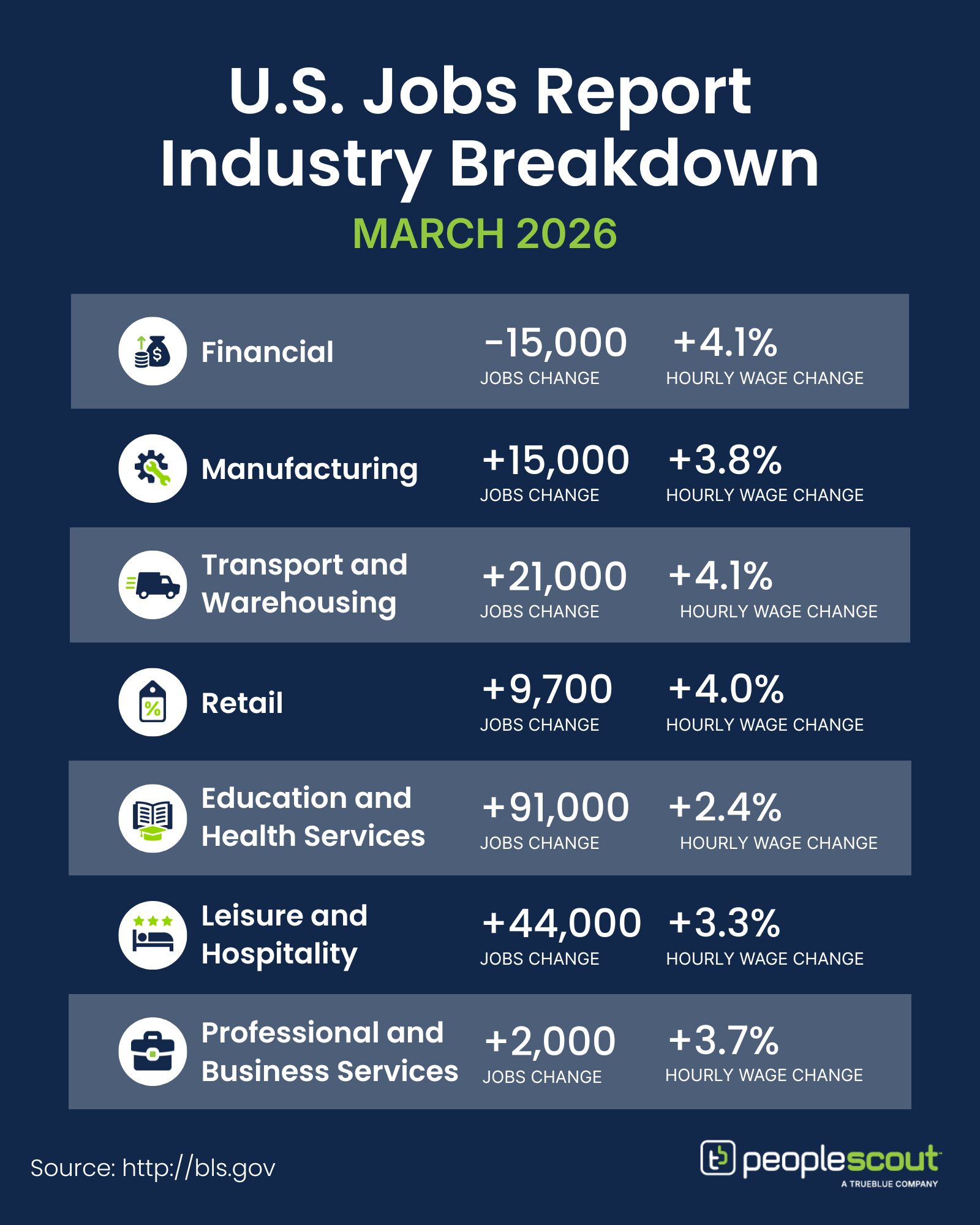

The March 2026 jobs report delivered a stronger-than-expected rebound, signaling renewed hiring momentum after last month’s sharp decline. U.S. employers added 178,000 jobs, while the unemployment rate edged down to 4.3%. Much of the improvement reflects the resolution of temporary disruptions impacting February’s numbers—winter weather and labor strikes—but the report also suggests underlying resilience in key sectors like healthcare and construction.

The Numbers

- 178,000: U.S. employers added 178,000 jobs in March.

- 4.3%: The unemployment rate declined slightly to 4.3%.

- 3.5%: Wages rose 3.5% over the past year.

The Good

March’s headline growth exceeded expectations and marks a meaningful recovery from February’s losses, suggesting the labor market retains underlying strength. Healthcare once again led hiring, adding 76,000 jobs. Construction (+26,000) and Manufacturing (+15,000) also posted gains, indicating that employers are still investing in infrastructure and production capacity where conditions support it. Importantly, layoffs remain limited—initial unemployment claims continue to sit near multi-year lows.

The Bad

Despite the strong headline, several indicators point to continued fragility beneath the surface. Wage growth slowed to 3.5%, and the average workweek declined, signaling softer earnings momentum and potential caution from employers. As in previous months, sector performance remains uneven. Financial services shed jobs, and government employment—particularly at the federal level—continues to contract. Long-term unemployment has also risen over the past year, and a sizable portion of workers remain underemployed, working part-time for economic reasons.

The Unknown

The March rebound raises an important question: is this the start of more consistent growth, or simply another data point in an increasingly variable cycle? Looking ahead, global dynamics will play a significant role. Rising energy prices and ongoing trade and policy uncertainty could weigh on business confidence and hiring plans in the months ahead. At the same time, structural factors—including an aging workforce and reduced labor force participation—continue to constrain labor supply. Additionally, many organizations are increasingly investing in technology and AI-driven productivity rather than expanding their workforce, reshaping both the pace and nature of hiring demand.

Conclusion

March’s jobs report offers a measure of reassurance after February’s decline. Hiring rebounded, unemployment remains contained and several key industries continue to expand. However, the broader picture remains one of measured, uneven growth. Slowing wage gains, constrained hiring activity and ongoing economic uncertainty suggest that employers are still operating with caution. For talent leaders, this environment reinforces the need for precision—targeting business-critical roles, optimizing workforce productivity and maintaining flexibility as conditions evolve.