The U.S. labor market closed Q2 2026 with hiring momentum slowing, but without the sharp deterioration many had anticipated. April and May delivered stronger-than-expected payroll figures before hiring declined in June, with just 57,000 new jobs added — the softest month of the quarter and well below the threshold most economists consider healthy growth. Yet unemployment edged down to 4.2%, and wage growth remained relatively steady, reflecting a labor market that continues to show resilience even as underlying dynamics shift.

The defining story of Q2 was not whether the labor market was growing or slowing, but the widening gap between headline stability and increasingly uneven conditions across industries.

Q2 2026 By the Numbers

- Unemployment: Q2 ended with the unemployment rate at 4.2%, edging down from 4.3% where it had held for most of the quarter. However, the decline was accompanied by a lower labor force participation rate, indicating that the improvement is not entirely driven by hiring activity.

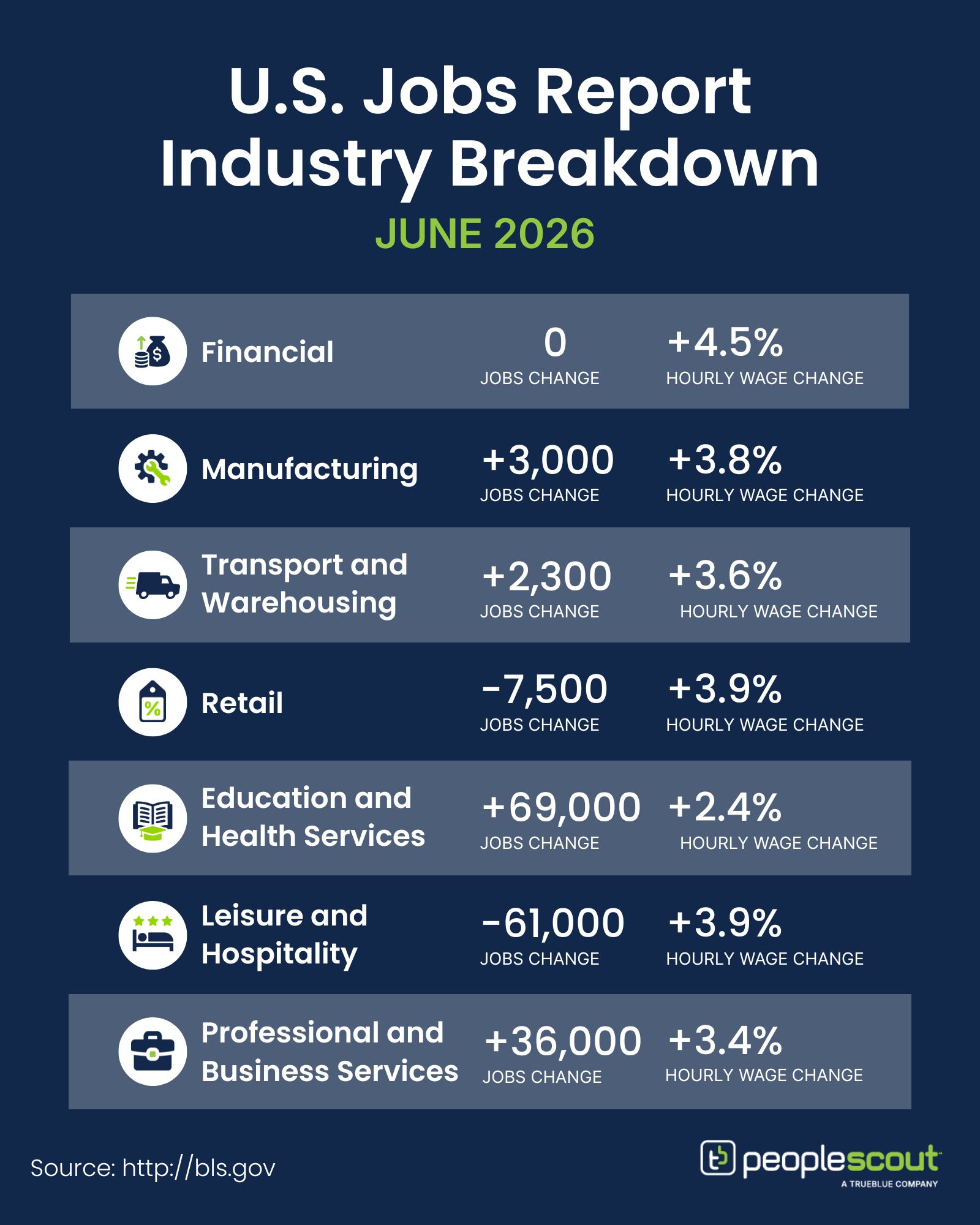

- Job Creation: Payroll growth followed an unpredictable path. April came in at 115,000 jobs before being revised upward to 179,000 gains. May delivered 172,000, followed by a significant drop to just 57,000 new jobs in June. Revisions to both April and May in the June report resulted in a net decrease of 74,000 jobs, tempering Q2’s overall growth picture.

- Wage Growth: Annual wage growth fluctuated within a narrow band throughout the quarter—3.6% in April, falling to 3.4% in May (its lowest level since 2021) before recovering slightly to 3.5% in June.

- Job Openings: After recovering to 7.15 million at the end of Q1 2026, openings rose to 7.6 million in April and held there through May — well above market expectations and the highest level since mid-2024.

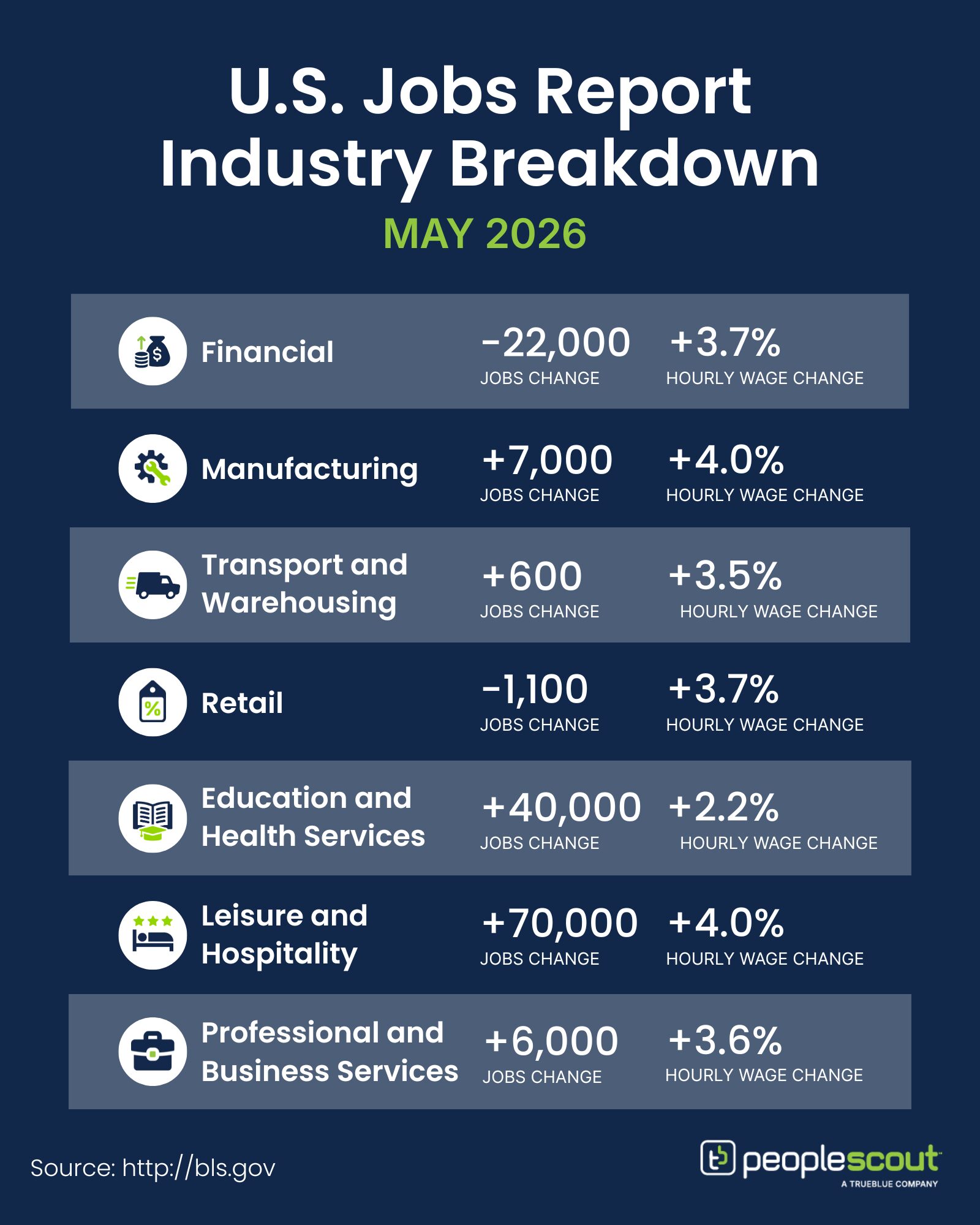

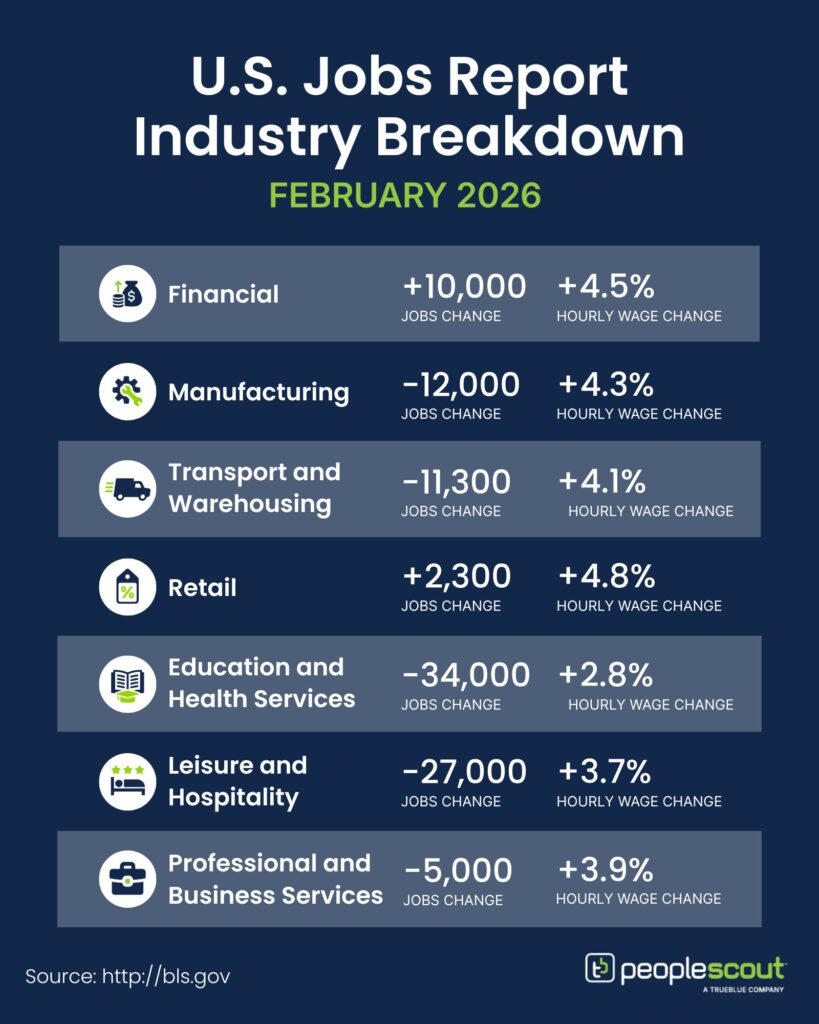

- Sector Standouts: Education and Health Services sustained the market across all three months. Professional and Business Services returned to growth in June (+36,000). Financial Activities recorded losses in April and May before going flat in June. Leisure and Hospitality swung sharply, surging in May (+70,000) before shedding 61,000 in June.

Top 4 Trends Shaping Q2 2026

1. The Market’s Mixed Signals

Q2’s central paradox was the disconnect between what the data showed and how business leaders felt about it. Unemployment fell, wages held steady and the economy continued to grow—yet CEO confidence fell from 59 in Q1 to 47 in Q2, tipping into negative territory for the first time this year, according to The Conference Board Measure of CEO Confidence™ survey. Nearly half of CEOs reported that economic conditions had worsened over the prior six months, and 40% expected further deterioration ahead. Hiring intent softened in parallel—31% of CEOs anticipated reducing their workforce over the next 12 months, up from 27% in Q1, while only 28% expected to add headcount.

The jobs data reflects some of that caution. June’s 57,000 payroll gain was the weakest of the quarter, revisions reduced hiring totals for earlier months, and the decline in unemployment came alongside declining labor force participation, underscoring that the headline figures tell only part of the story. The market is not deteriorating, but the gap between what the numbers show and how employers are responding appears to be widening.

2. The Load-Bearing Role of Healthcare in a Slowing Market

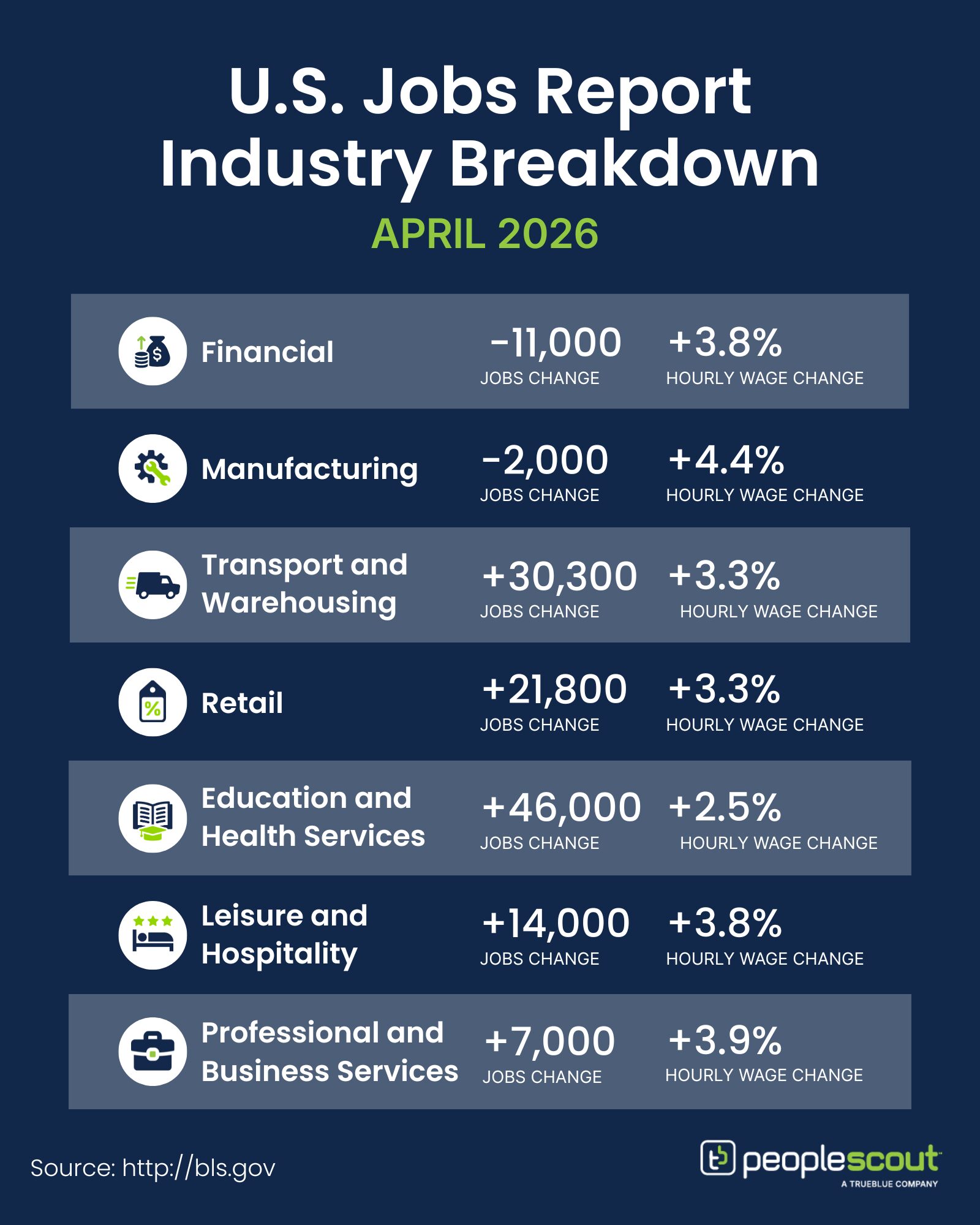

If Q2 had a single structural constant, it was the outsized contribution of Education and Health Services to overall job creation. Healthcare added 37,000 jobs in April and 35,000 in May, while the broader Education and Health Services sector added 69,000 in June, balancing net job gains as other industries declined. Without this sector, Q2’s employment picture would have looked considerably weaker.

The drivers behind this sustained demand show no sign of easing: an aging population, persistent shortages of clinical and allied health professionals, and roles that depend on human interaction, clinical judgment and physical dexterity. While other sectors are evaluating whether technology can absorb capacity, healthcare continues to rely heavily on people.

3. The AI Efficiency Overhang

The impact of AI on employment is not arriving as a sudden wave of displacement, but rather as a quiet, selective reconfiguration of where and whether headcount gets added. Financial Activities recorded losses in both April and May before flattening in June. Information services shed positions in April. Major employers including HSBC and Mizuho have signaled longer-term reductions in administrative roles, typically framed as reallocation toward higher-value work. A survey of 750 CFOs projected a modest but uneven 0.4% net headcount decline across 2026, with the burden falling disproportionately on office support functions.

The JOLTS data adds a further dimension. April’s surge in job openings was concentrated almost entirely in Professional and Business Services (+668,000), yet actual hiring in the sector (+7,000 jobs) remained subdued. Openings are staying on the books longer not because demand is booming, but because workers are not moving. The quits rate, at 1.9%, sits well below its pre-pandemic range, reflecting a workforce that feels it has fewer options. The result is a market that looks active on the surface but is experiencing considerably less actual movement than the headline openings figure implies.

4. The Hidden Cost of Wage Cooling

On the surface, Q2’s wage trajectory looked stable—annual growth held within a narrow 3.4–3.6% band throughout the quarter. But wage growth continuing to trail inflation means many workers’ earnings are not keeping pace with the cost of living, and sentiment data reflects that reality. Just 28% of Americans believed it was a good time to find a quality job, down from 70% in mid-2022, with college graduates particularly pessimistic at just 19%. The subdued quits rate reinforces the picture—workers are staying put, but out of caution rather than satisfaction.

Against this backdrop, the U.S. gender pay gap widened for the second consecutive year, with women now earning 81 cents for every dollar earned by men—the first back-to-back increase since the 1960s. The combination of stagnant real wages, declining worker confidence and widening pay gap is creating employee experience conditions that will increasingly test retention strategies.

What This Means for TA Leaders

Q2 delivered a market that held together without accelerating, and talent strategies must operate in the gap between stability and growth

Anchor hiring decisions in business outcomes, not market momentum. Lower CEO confidence means headcount decisions will face greater scrutiny from leadership. TA teams that can quantify the ROI of specific hires—rather than pointing to market conditions as justification—will carry more weight in H2 planning conversations.

Healthcare and specialist talent competition has no near-term ceiling. The sector that sustained Q2’s employment picture faces the same structural shortages it did entering the quarter. For any organization dependent on clinical, allied health or care-facing roles, proactive pipelines, internal mobility pathways and education partnerships are becoming prerequisites rather than differentiators.

Audit which open roles are being filled. The AI efficiency overhang isn’t showing up as layoffs—it’s showing up as headcount held open and job functions quietly redesigned. Knowing which vacancies reflect genuine demand versus roles being absorbed by productivity tools is increasingly a core workforce planning competency, not a nice-to-have.

Treat declining sentiment as a leading retention indicator. Wage growth trailing inflation, worker pessimismand a widening gender pay gap don’t generate visible attrition spikes immediately—but they erode engagement over time. Total rewards transparency, equitable pay practices and meaningful career development conversations are retention strategies now, not value commitments for better conditions later.

Q2 delivered a labor market that is slowing without breaking. For talent leaders, the strategic response is not to wait for clarity—it is to build workforce precision, pipeline depth and organizational agility to perform effectively for whatever lies ahead.